Photo courtesy of Daily FT

At a small grocery store, an elderly man pointed at a particular packet of biscuits and asked what the price was – it was Rs.70. The man asked if there were biscuits for Rs.50 in the store and the cashier responded, “Everything we have is above Rs.60”.

Inflation rates and the cost of living have become part of people’s daily worries. According to the Department of Census and Statistics (DCS), inflation rates increased from 4.1% to 18.7% from March 2021 to March 2022. Both food and non-food items have been drastically affected with food items being affected more with price hikes as high as 30.2% compared to March last year, as opposed to non-food items that has a hike of around 13.4%.

The inflation rate has been impacted by several factors. The Central Bank’s decision to implement an expansionary monetary policy by printing money to finance the budget deficits was one of them. Two other factors were the cost-push inflation and demand-pull inflation to food prices. Cost-push inflation is the increase in prices due to lack of supply caused by curtailing imports and policies such as the fertilizer ban that reduced the supply of goods. Demand-pull inflation is the increase in prices due to higher demand. Even with insufficient money, due to lack of supply, the prices increase given the supply doesn’t meet the demand. There is insufficient data to pinpoint which one of these factors had the greatest impact but in combination they have resulted in heavy burden on the general public in terms of their wellbeing and access to essential goods and services.

Assuming the rupee stays afloat, imports would be relatively expensive in general. Given the increasing risks to agriculture output due to the fertilizer ban, lack of fuel and uncertainty of weather patterns, the price of food products could become unbearable for the poor in the coming months. While it is not only the poor who are struggling to adapt to these dire economic conditions, the outcome of these erratic economic policies affects them the most. The lack of electricity (which affects households and employment) and the sky rocketing price of alternative fuel for cooking (firewood and kerosene oil) make living extremely difficult for the poor. The effect of these policies are felt by all strata of society; however, the lack of an income buffer/savings, combined with significantly low income (which is sometimes further strained due to low economic activity in the economy) impacts the poor substantially.

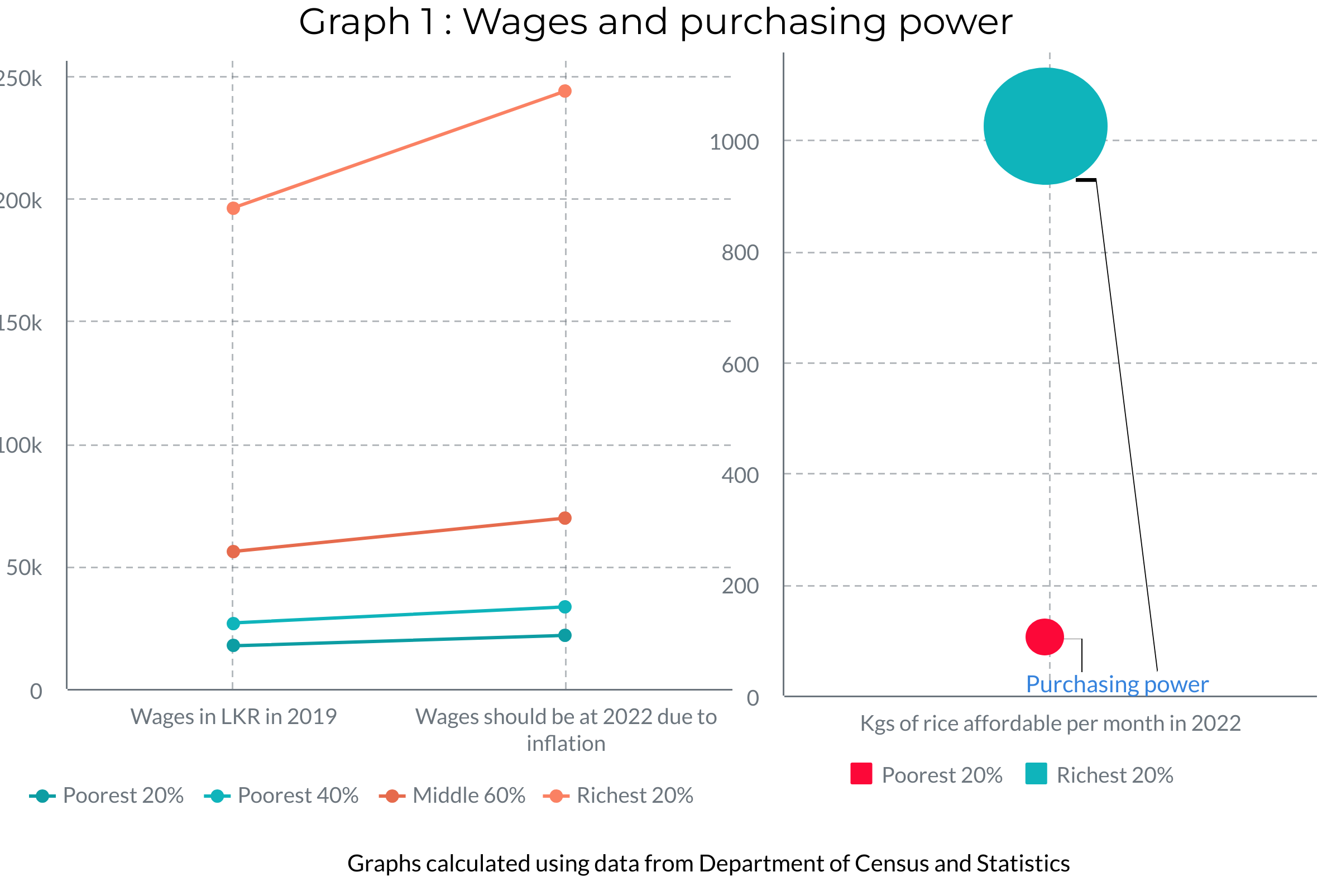

As a result of inflation, the purchasing power is reduced drastically over time. Imagine what would happen if prices rose by about Rs.30 for a kilo of rice once a week[1]. A Rs.30 increase in price within a week would mean an increase in the expenditure of the poorest 20% from 8.2% to 9.5% as a percentage of their income[2]. That’s an increase of 1%.

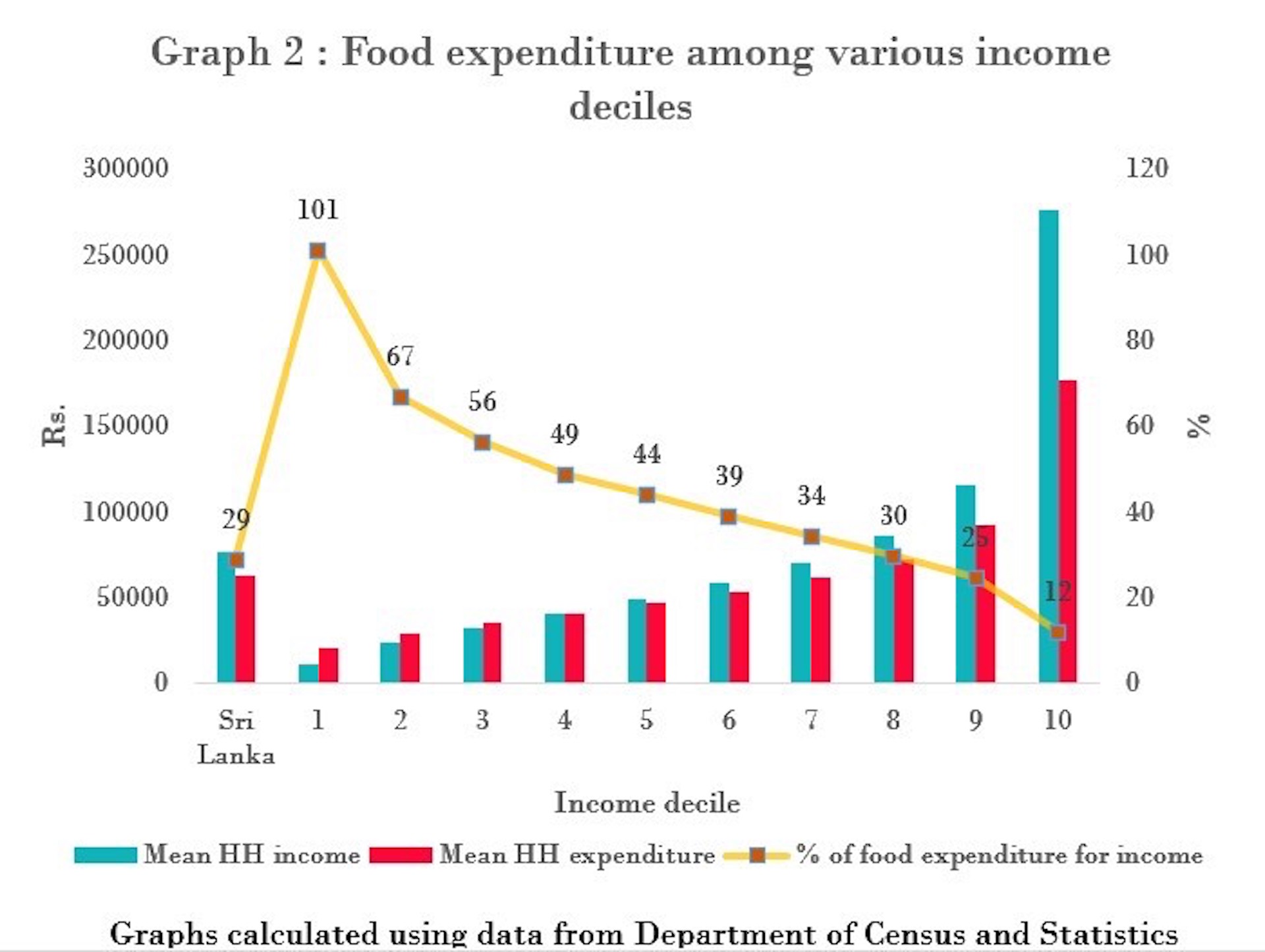

The main reason for non-affordability revolves around wages. More often than not, the wages of the poor are informal, fixed over a long term period and are informally negotiated. Those in other income tiers, especially those with more formal types of employment, often benefit from inflation adjusted wages. Therefore, for those with constant income on the lower end, regularly fluctuating prices reduce purchasing power but also results in higher expenses on food. As the poor anyway spend a larger share of their income on food (refer graph 2), this situation of inflation and fixed wages will see an increase in income disparity between the rich and the poor.

According to the DCS the 2019 Household Income and Expenditure Survey shows that 101% of the income in the first income decile and 67% by the second income decile was spent on food. What is even more cause for concern is that up to the third income decile (that is people earning less than Rs. 36,381[3]), the overall expenditure exceeds the income earned. Thus, two years on with similar or slightly adjusted wages, the high inflation rates make the situation more aggravated. As a coping mechanism the expenses are financed through means such as pawning assets, microfinance and other types of loans. According to a non-representative survey done by the Centre for Poverty Analysis (CEPA) during the first wave of the COVID-19 pandemic (data collected for a month up to 2020, May), the lowest income (less than Rs.50,000) group has resorted to more than four means of other resources such as cash at bank, cash at home, engaged in a secondary job, pawning jewellery and obtained cash from others with and without interest. The fact that they have already resorted to these schemes so early on means that going forward they will have fewer options and more debt burden, a grim situation. It also highlights the lack of adequate social protection schemes that can cover for prolonged periods of stress.

In a survey done by CEPA in June 2021 targeting fishing communities (post the X-press Pearl disaster) there is evidence that this community hit by both COVID-19 and the shipping disaster did reduce or change food consumption patterns but tried to continue with similar levels of expenses for education and health. As the economic crisis worsens and continues for a longer period of time, it is likely that further ripple effects will be seen by pushing people not only to consume less food but to reduce other expenses on education, health, housing and electricity. This deteriorates their long term wellbeing.

While Sri Lanka does face an uphill challenge, the way forward cannot lose sight of the poor and their wellbeing. Policies must support lower income tiers in terms of adjustable wages and safety nets. Moving ahead with tax reforms and starting off with re-imposing income taxes can provide the needed finances for social protection schemes for the poor. These schemes have to be adjusted to reflect the new situation – the present financial needs as well as the target group. We know that it cannot be one off packages like the recently concluded COVID-19 relief package (Rs.5,000 and a package inclusive of staple items), which is inadequate to deal with long term stresses. A more integrated approach with a strategic overall objective recognizing and addressing vulnerabilities while identifying needs such as food but also access to health, education, electricity, transportation and accommodation in a more integrated fashion could increase efficiency.

The government and development actors need to take necessary measures to collect sufficient data to implement and monitor these policies and programmes. The current lack of data on COVID-19 driven poverty conditions is a clear example of the need for more real time data.

It is necessary for Sri Lanka’s way forward to duly consider the needs of the poor with high emphasis on social safety nets. With tighter conditions and limited economic growth, it is imperative to ensure income redistribution and more equitable economic growth strategies are formulated.

[1] Calculated using retail prices from Department of Census and Statistics published for the 1st week of April 2022 for Samba (average) (203LKR-178 LKR)

[2] Calculations based on retail prices between 4th week of March and 1st week of April

[3] According to the income decile

This article was first published on the blog.